Launching a medical clinic requires careful financial forecasting to ensure long-term sustainability and profitability. It enables aspiring clinic owners to estimate the initial investments needed to cover capital needs and potential early operational losses.

A robust financial plan allows clinic founders to not only project revenue and resource needs but also help facilitate informed decision making that support ongoing sustainable growth and minimizes risks.

A well-structured financial foundation enables startups to allocate resources strategically so that the clinic can focus on delivering high-quality care. This section explores key financial planning principles, including budget development and financial forecasting.

Stepwise Financial Forecasting Best Practices

Before the initial financial needs can be forecasted, founders must have a good idea of the services that will be offered and what is needed for the operations. This may require discussions with mentors and other clinic owners.

Once there is clarity about the services that will be offered, the following steps can help structure the approach to forecasting:

1.Begin by identifying the start-up needs

- When thinking about your services, define the Minimum Viable Product (MVP) as well as the “dream” version. The MVP would be the services you would be starting with before adding other services (which you may have less certainty about)

- For each version, think of the clinic’s functional spaces and identify:

- What equipment or furniture is needed

- What IT systems need to be installed

- What providers need to do their job

- What the MOAs need to function

2. Estimate your start-up costs

- Budget conservatively, when in doubt estimate higher

- Think about the space and equipment needs granularly; draw a floor plan and fill each room with all the equipment, IT needs, and furniture you plan

- Think about your supplies at higher level; here the goal is to identify how much supplies might need to be purchased to ensure smooth operations in the first quarter

- This downloadable excel document may help get you started

3.Forecast Operational revenues and expenses and estimate the income and loss

- What are the operational revenue streams when everything is running at capacity?

- What are the expenses that enable revenues, when fully functional?

- Connect variables that travel together

- More information on common revenues and expenses are provided in sections below

4.Model the ramp-up period

- How long would it take to get to full functionality?

- How long to recruit and onboard providers

- For each quarter during the ramp-up period, what are the revenue and expense expectations?

- How much financing may be needed to cover losses during the ramp up?

Depending on founder experience and familiarity with budgeting, it may be beneficial to connect with a business consultant with a focus on healthcare to help develop a forecast. Budget and financial management templates are available for reference through Microsoft Platforms.

The sections below explore the common revenue and expense categories of primary care clinics. They may be helpful in guiding financial forecast and budgeting .

Estimating Clinic Revenues

Generally, depending on the corporate structure, clinics may generate revenue from operations of the primary care clinic as well as from other non-primary care operations (renting spaces, financing activities, etc.). In this section, we focus on the (primary care) operating activities.

Operating Revenue Streams in a Medical Clinic

In most community primary care practices, the main revenue stream is the overhead collected from (or on behalf of) providers.

- For NPs, the overhead is currently outlined as part of their contract and may vary slightly depending on the region and setting.

- For RNs and allied health professionals (such as social workers, counsellors, etc.) who provide services as part of a Health Authority initiative (such as PCN), the clinic will receive a set overhead based on practitioners Full Time Equivalency. If these professionals are hired by the clinic independently, the income generated from their services will go to clinic, who is responsible for their salary.

- Physicians, specialists, and other providers who bill MSP, third party insurance or private billings will pay overhead based on a remuneration agreement. These agreements may also apply to NPs in future if the nature of current contracts changes. The most common remuneration models in BC are discussed below.

In addition to overhead collected from providers, medical clinics may leverage other income streams including:

- Additional operating revenue streams

- Medical legal, third-party billings WCB, ICBC, etc.

- Group visits/programs

- Health authority/ministry initiatives

- Private procedures performed by technicians or providers

- Non-Rx dispensing and related wellness offerings

- Additional non-operating revenue streams

- Renting spaces during non-peak hours

- Research and data sharing funding

- Charitable donations provided to the clinic (depending on the clinic entity)

It is important for founders to diligently consider the revenues generated from overheads and other streams. The main question a clinic owner should consider is whether the revenue generated is enough to at least cover expenses (and a reasonable operating buffer).

Common Remuneration/Overhead models in BC

Medical clinic often needs to balance the revenue needs with recruitment and retention incentives for providers. The scope of the remuneration agreement may differ for different types of providers that the clinic aims to recruit. For example, physicians, specialists, psychologists, and some allied health providers such as Physiotherapists usually pay overhead for both MSP and non-MSP covered billings. Others, such as NPs, have allocated overhead amounts for activities outlined in their contract (e.g. PCN agreement) and may only have remuneration agreements for the portion of earnings related to activities not governed by their contract.

This section aims to provide examples of remuneration structures commonly used in BC and briefly discusses pros and cons of each structure. Please note this is not an exhaustive list and those interested in a remuneration model should conduct further due diligence. The most common remuneration models in BC are discussed below.

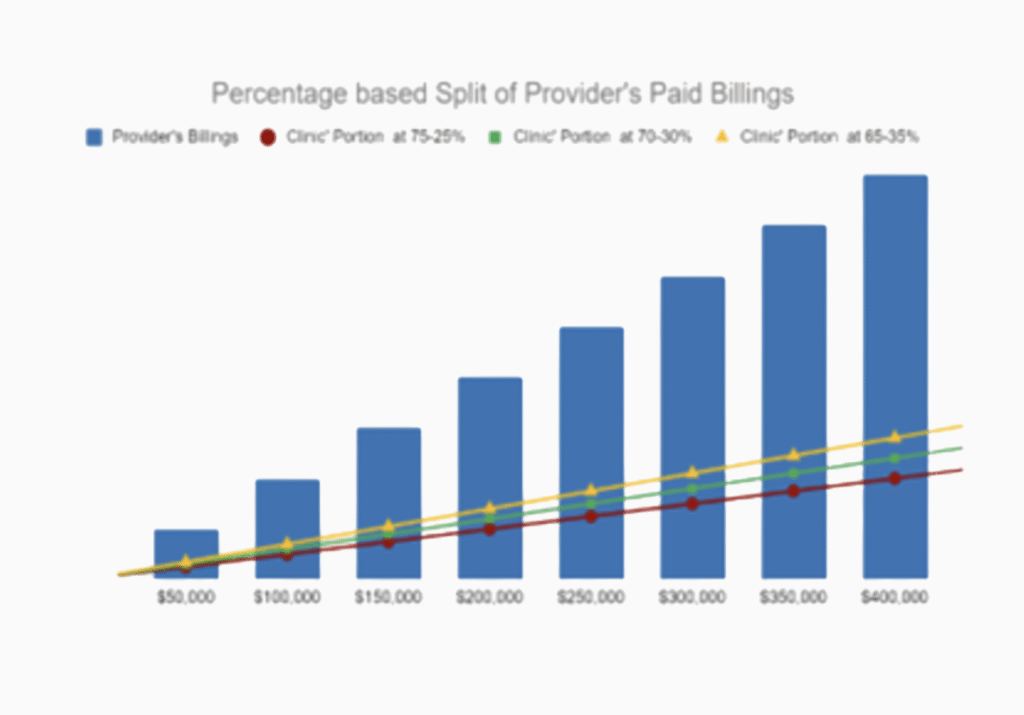

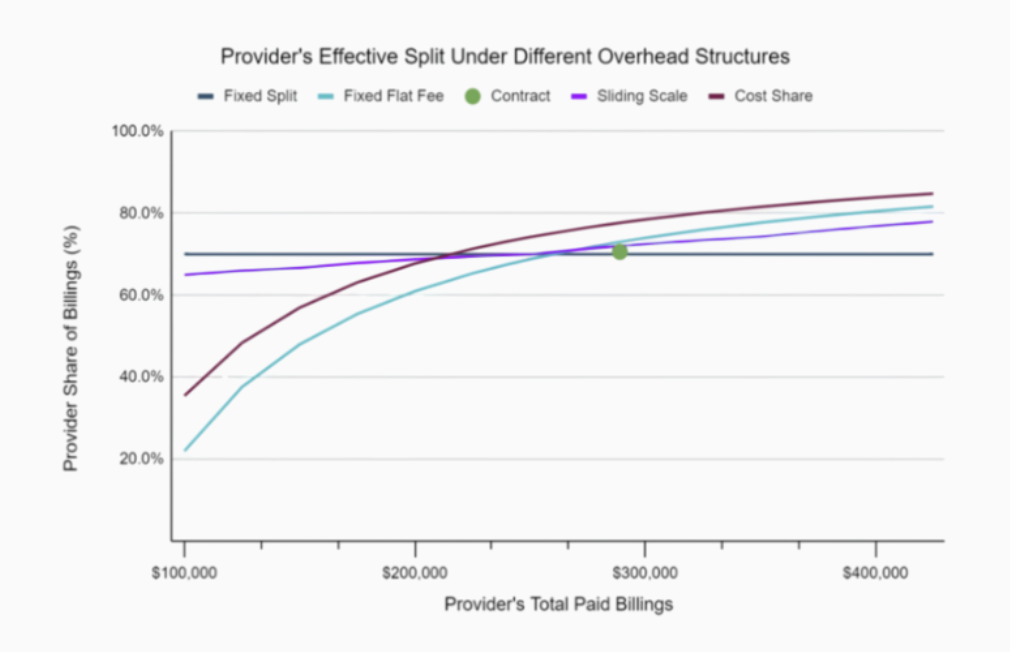

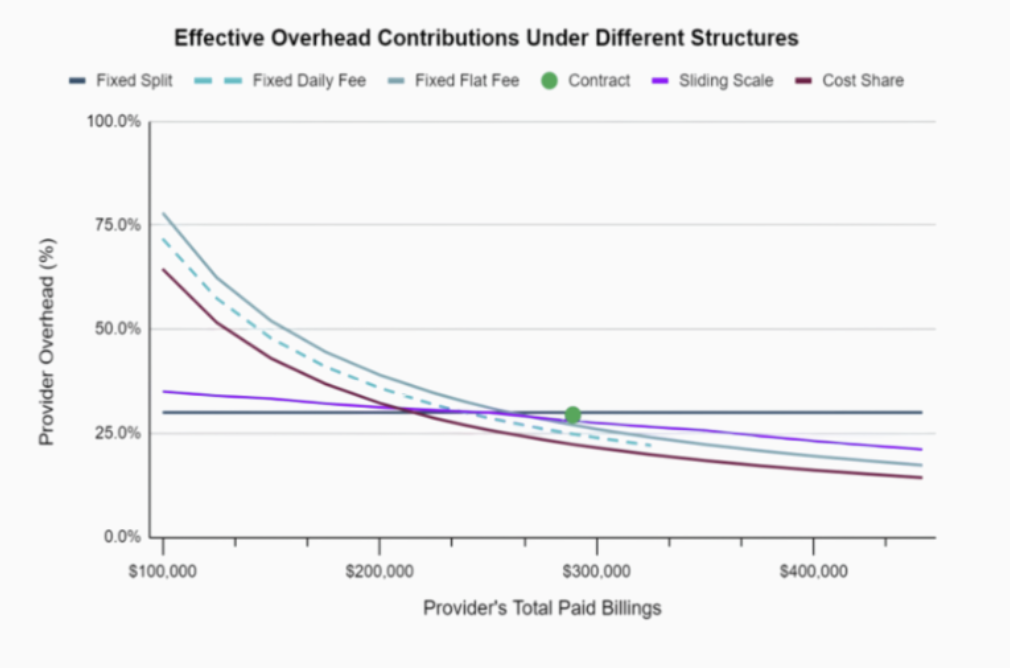

Fixed Split (a.k.a. % Based Split)

In this model, the clinic collects an agreed upon percentage of each provider’s paid billings. For example, in a 70-30 split, the provider pays 30% of their paid billing to the clinic to cover overhead and keeps 70% as earnings. As the graph below demonstrate the clinic revenue is dependent on the provider earnings.

In this overhead structure, unless otherwise outlined in a contract:

- Efficient billers may pay more in billing than those less efficient

- The clinic bares the risk associated with unexpected absences or unfilled rooms

- Clinic owner(s) have an interest to find locums

- Fluctuations in provider schedule can significantly impacts the clinic’s financial outcome and sustainability

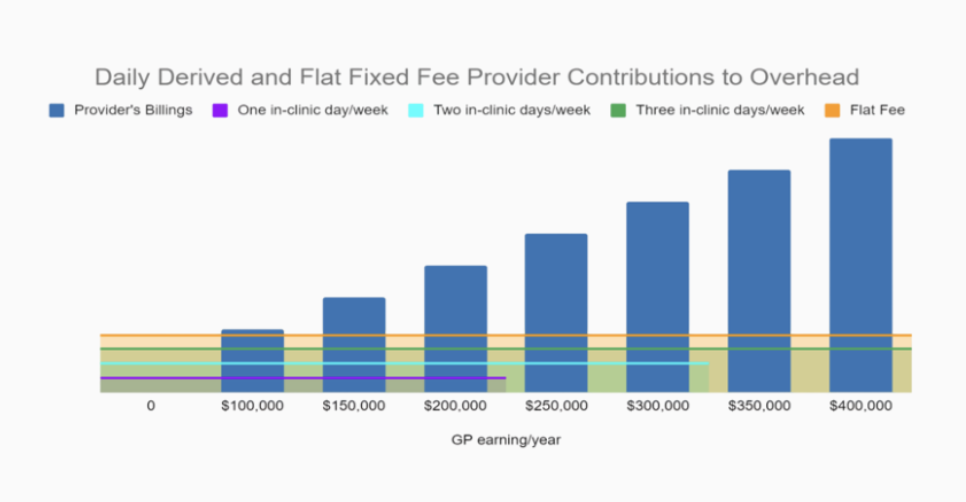

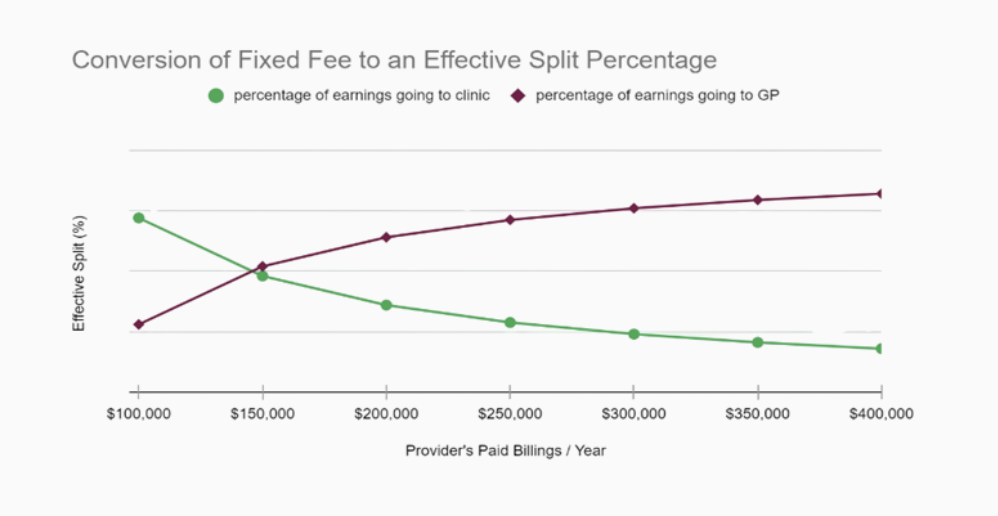

Fixed fee

As the name suggests, in this remuneration model, the clinic collects a fixed fee from each provider (usually at the beginning of each month) to cover the clinic’s overhead. The fee is usually calculated based on the number of days the providers commit to working at the clinic. Provider work commitments may be revisited once or twice a year as outlined in their agreement. The graphs below demonstrate that provider billing does not affect the anticipated clinic revenues. When compared to fixed split this model may be more appealing to higher billers.

In the fixed fee overhead structure:

- If a provider decides to reduce their practice days within the agreement period, they are still responsible for the fixed payments

- It is to providers’ benefit to ensure locum coverage

- High billers can usually retain more of their earnings

- The clinic has certainty in revenues, despite variability in provider billing

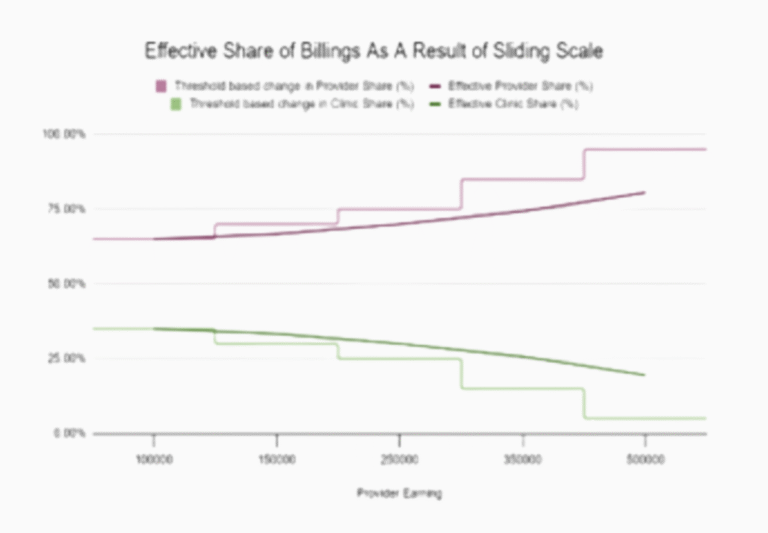

Progressive % of billing (a.k.a. Sliding Scale)

In the model, the provider contributes a progressively reducing percentage of billing to the clinic. This system is comparable to the reverse of our progressive tax system. As provider billing levels increase, the percentage of overhead attributed to the clinic reduces. This is accomplished by charging a reduced overhead for a predefined segment of the billings. This model is sometimes seen as a compromise between the fixed split and fixed fee models. As the graph demonstrates the effective overhead reduces as the provider billing increases. The clinic forgoes some of the upsides seen in fixed split but also gains some protection against unexpected downside.

In the progressive % of Billing model:

- Both parties will benefit if there is consistent locum coverage

- High earners keep more of their earnings and low earners pay a higher percentage

- May not be ideal for those who work less than 0.5 FTE or those who do not bill a lot

- Clinic still faces risks if providers depart for extended periods of time

Cost Share

In a cost share model, the clinic aims to recoup only its expenses and a small operating buffer. Expenses, and therefore overheads, are usually calculated based on relative clinic usage (days of work). This means the providers pay a monthly fee, calculated based on historical values, and as financial information comes in, the providers’ overheads are re-settled or down.

In cost share model:

- The effective overhead is usually less than other models, which helps recruitment and retention

- Everyone at the clinic has an interest in ensuring the patient’s needs for access are met

- Providers usually divide oversight of the clinics among each other to ensure equal workload

- Unless actively planning for future costs, the renovation and capital costs can result in a significant increase in overheads in particular years

- As expenses grow, so do overhead expectations, which may make it difficult for providers to plan their personal finances.

Graphical comparison of the remuneration models

As shown below, the effective overhead can vary significantly depending on the selected remuneration models. In most cases, the providers and clinic interests may seem opposing. It is important to both parties to approach remuneration discussions transparently and with both of their interest in mind, so that a reasonable compromise, benefiting both parties, can be achieved.

Other Useful Resources Related to Clinic Revenue

- NP Overhead

- Encounter and Shift Coding

- Third party Billing

Estimating Clinic Expenses

Accurately estimating expenses is a critical step in launching and managing a successful medical clinic. Like revenues, clinic expenses can be broadly separated into operating and non-operating expenses. Primary care operating expenses can be segmented into three types:

- Fixed Expenses– remain constant regardless of the number of provider sessions (and patients) of the clinic. Whether a provider works in-clinic or remotely they should be covering a share of these expenses through their overhead.

- Location Agnostic Variable Expenses – change as number of provider (and patient demand) sessions increases or decreases. This category of variable expenses will be affected whether the provider is working remotely or in clinic. Therefore, providers working in any capacity should help cover these expenses through their overhead. and categories of expenses.

- In-Clinic Variable Expenses– also changes in value based on the number of provider sessions, however this category of variable expenses is only affected when providers are working in-clinic.

The following represents the clinic expense line items commonly seen in bookkeeping and financial documents, segmented into expense types. Limited examples of non-operating expenses are also provided below.

Operating Expenses

Fixed Expenses

- Space expense (lease, utilities, taxes, strata, etc.)

- Maintenance and repairs

- Janitorial, cleaning, and waste disposal

- Security/security system

- Parking

- Licenses, insurance, and permits

- Internet

- Computer, technology and IT

- Fax

- Telephone

- Equipment purchases or lease

- Website, advertising, and marketing

- Professional services

- Recruitment and retention

- Interest and bank charges

- Management and administration

- Miscellaneous and incidental

Non-Operating Revenues and Expenses

- Bad debts

- Amortization & depreciation

- Loan repayment

Location Agnostic Variable Expenses

- Wages, benefits, and bonuses

- EMR

- Software subscriptions

- Uniforms

- Courier services and postage

- Meals and entertainment

In-Clinic Variable Expenses

- Medical supplies

- Office supplies

- Interest

- Income taxes

- Capital investment costs

Despite the considerable number of expense categories, there are five categories that represent the most significant expense drivers. These include:

- Staff wages, benefits, and bonuses (on average between 50 to 60% of total expenses)

- Space expenses (on average between 15-25% of total expenses)

- EMR (on average between 4-6% of total expenses)

- Medical and office supplies (with combined average between 3-7% of total expenses)

- Janitorial, cleaning and waste disposal (on average between 2-4% of total expenses)

The staff and space expenses accounts for approximately 75% of total expenses. This highlights the importance of ensuring optimal utilization and detailed forecasting of these two categories. Comparatively other categories may not have as significant of an impact on overall success of the clinic.

Strategies for improving staff utilization and management are discussed in HR Planning and Management <link to section 4>. The next section briefly discusses strategies for space planning to help improve space utilization.

Space Planning

A critical factor in your strategic planning is deciding on what type of space you need. Subsequently, it is crucial to find a space that meets your strategic plan, long term goals and the business plan you have developed without over committing. Larger spaces are not always advantageous. They represent higher space costs that may need to be amortized over larger number of providers sessions, which in turn can require higher staffing costs.

This section provides tips on finding the location and tips and check list to get you started with designing the space.

Finding a suitable location

The commercial building you choose will have a significant impact on your business. Ideally, its size, layout, location, and appearance should all enhance your operations while respecting zoning and environmental regulations. Although a clinic founder may consider purchasing a commercial property to house the clinic, the clinic would still need to pay lease to a landlord (even if the landlord is the founder).

This BDC article on how to choose the right location for your business suggests considering the following five elements when searching for the right location for your business.

- Adapt your selection to the needs of your business

- Does it require modification?

- Consider local taxes and infrastructure

- Allow for future growth

- Separate your needs from your wants

Once you have identified suitable spaces, you may need to consider your lease agreement. Most commercial lease agreement in BC are triple net (NNN) leases. In this type of commercial lease agreement, the base rents are lower, because the tenant is responsible for paying three key expenses in addition to rent:

- Property Taxes – The tenant covers all real estate taxes associated with the leased property.

- Building Insurance – The tenant is required to pay for insurance coverage on the property.

- Maintenance Costs – The tenant assumes responsibility for strata fees, upkeep, repairs, and general maintenance.

Pricing is usually provided as annual or monthly base rent price per square foot of space. And the other expenses (such as property taxes and strata fees may be charged monthly or quarterly). It is always a good idea to seek the advice of an independent commercial real estate advisor who can help you set criteria for choosing the right building. This advisor should know the area and be familiar with zoning regulations and any potential issues concerning the building, its location or uses to which it may be put.

Those interested in further information may want to review the following additional resources:

Best Practices for Primary Care Clinic Space Planning

It may be difficult to find a location that is already designed to fit the medical clinic needs. Therefore, it is common for founders to make limited renovations. To help optimize the space utilization, it may be helpful to:

- Design standardized rooms, so that any clinic provider may be able to work out of any room.

- Think about clinic flow and place MOA stations in areas that reduces unnecessary back and forth (if your clinic will have a support MOA, a station in the hallway may be advantageous).

- Consider having a large, shared, provider office instead of many small ones that may sit empty.

- Think about designing multi-use spaces. Kitchen and staff seating area could double as meeting room. Reception could serve as group visit area in the evenings.

- Design protected spaces for staff who do not need to perform patient facing tasks, to allow them to focus on their activities.

- Consider setting aside a small office for a few virtual care spaces, that are separated by sound absorbing panels. This will prevent providers from using exam rooms for virtual care meetings.

In addition to thoughtful design, space utilization can be improved through purposeful scheduling of shifts. Many clinics empower providers to work in-clinic for half-day sessions. If that is a desired policy, ensure the remainder of the time are usable for others. For example, if a provider works from 9 am to 1 pm, others can utilize the same room from 1 to 5 pm. However, if an NP occupies the room from 11 am to 3 pm, it would be considerably harder for others to plan to use the room before 11 am or after 3 pm.

Minimizing the clinic footprint and maximizing the exam room utilization may make the difference between a financially successful clinic and an unsustainable one. Planning the space and the schedule are crucial elements for a successful clinic.

Other Resources related to Expenses

Individual NPs may have some of the expense categories highlighted above. Some of these are highlighted in this NNPBC Anticipated Costs for Self Employed NPs document.

Bookkeeping Best Practices and Related Resources

Effective bookkeeping practices are essential for maintaining financial stability, ensuring compliance, and reducing risks. Some key best practices are shared in this section.

Separate Business and Personal Finances

- Open a dedicated business bank account to simplify bookkeeping and tax reporting.

- Use corporate credit cards for clinic-related expenses to help maintain clear financial records.

Maintain Accurate Records

- Create a Chart of Accounts (COA) using the common revenue and expense item provided in the estimating revenue and estimating expense sections above. Use these categories to track transactions in the general ledger.

- Keep detailed records of the assets, liabilities, revenue, expenses, and equity to ensure accurate bookkeeping and reporting. Work with an accredited accountant to clearly designate how to account for common expense and revenue items.

- Retain financial documents for at least six years, as required by the Canada Revenue Agency (CRA).

Leverage Accounting and Banking Software

- It may be helpful to select a cloud-based accounting software like (e.g. QuickBooks, Sage, etc.) to streamline financial management.

- Ensure accounting software integration with Electronic Medical Records (EMR)

- Set-up online banking to allow for easier review of transactions

- Set-up electronic funds transfer (EFT) and other payment systems

- Integrate baking software with your accounting software

Track Revenue and Expenses of Different Functional Streams Separately

- Organize the revenue and expenses for each functional stream (primary care, allied health, specialized services, private procedures, etc.) Separately.

- Regularly reconcile accounts to ensure accuracy and prevent discrepancies.

Stay on Top of Payroll & Tax Obligations

- Depending on the number of staff, it may be beneficial to use payroll management tools (e.g. PayWorks, Rise, Wagepoint, etc.) to handle staff salaries, benefits, and deductions.

- Become familiar with GST/HST exemptions for medical services and ensure compliance with tax regulations.

Onboard a Point of Sales System and Automate Private Billing and Invoicing

- If patients pay for some services, consider onboarding a Point of sale (POS) system. It may be helpful to review this POS selection guide .

- Implement automated invoicing and payment reminders to reduce administrative workload.

- Regularly review accounts receivable to minimize outstanding payments.

Conduct Monthly Reviews and Reconciliate Accounts

- Match bank statements with clinic financial records to help identify errors early.

- Perform quarterly financial reviews to assess clinic performance and cash flow against previously prepared budget.

- Periodically review the DoBC’s Internal fraud and financial control checklist

Click here for section D: Clinical and Medical Oversight